For reading and commenting on earlier drafts, I’d like to thank Nic Carter, Christian Angelopoulos, Noah Jessop, Chris Chow, Rooter, Jack Dille, Brandon Iles, Fiddlekins, Matt Fisher, and Joey Roth. All errors that remain are entirely their fault.

Introduction

“You can flee natural calamities but cannot escape the consequences of your own sins” (天作孽猶可違, 自作孽不可活), said Mencius in the Venerated Documents.1 Commentators have described the failures of Silicon Valley Bank (SVB), Silvergate Bank, Signature Bank, and Credit Suisse in terms ranging from the technical to the dramatic. Bailout. Crisis. Hyperinflation. Collapse. Fog of War.2 Still, it is hard to not see SVB’s failure and the crisis of our banking system in general as the inescapable consequences of our regulatory sins.

History suggests that far from reducing the frequency and intensity of financial crises, government interventions lay the foundation for more crises in the future. And it is our inability to tolerate the consequences of a reduction in debt that has allowed intervention to become a political reflex. This three-part series explores the future of banking and whether it will still be “banking” in any recognizable way. But before we do so, we will first explore the self-reinforcing and seemingly inescapable cycle between crisis and intervention which has allowed the banking sector to grow to massive proportions, saddling societies with misallocated capital and sapping economic vitality.

A famous dictum from the one of the Five Classics.

Spark in the Tinderbox

A number of prominently online VCs such as Matt Ocko think that “without the publicity & sense of urgency that each of Garry Tan, David [Sacks], Jason [Calacanis], & many others created, the powers that be may very well have stayed asleep and f’ed the country.” Predictably, they have been mocked for thinking their Tweeting saved the financial system (see below). Calacanis, Sacks, and others claim that jealous anti-tech masses objected to the SVB bailout because they wanted to see tech fail.

Spiderman saves US financial system with his Tweets.

Others, like investor Keval Desai, take a different view. “Oh the irony of today’s VCs who are calling for a govt bailout who yesterday asked their cos to pull out & caused the run in the first place.” He’s not entirely wrong. For four decades SVB was the major banking partner to the venture capital industry and their portfolio of high-tech startups. Nonetheless, two high-profile venture partners precipitated the bank run. Garry Tan, president of Y-Combinator, messaged over 1,000 portfolio companies, suggesting they pull cash from SVB.3 Founders Fund did the same, helping spark a “Twitter-led bank run.”4

Can history help us decide who is right, Ocko or Desai?

Detroit's Bank of the Commonwealth, in the upper left corner of the image.

Today’s banking failures resemble the banking failures of the 1970s, when Federal Reserve chairman Arthur Burns repeatedly tried and failed to get inflation under control. This was the beginning of the “too big to fail” era, starting with Detroit’s Bank of the Commonwealth in 1972. Like SVB, it too bought long-dated government bonds after deposits tripled in preceding years. The Federal Deposit Insurance Corporation (FDIC) bailed out Commonwealth on the grounds that it was essential to “service to the black community in Detroit,” a legal basis conjured out of thin air. As bigger banks began to fail, federal regulators found themselves bailing out all manner of regional banks, consolidating them into larger beasts “too big to fail.”

In light of that history, saving SVB uninsured depositors was almost certain, though not because problems at VC-funded moonshot startups, which have a failure rate of ~95% anyways, would bring down the economy. This suggests that, as General Catalyst’s Hemant Taneja commented, “Panic wasn’t the way to handle it.”5

VC: My work here is done. FDIC: But you didn't do anything.

When in a tinderbox, it is best to tread carefully. Telling thousands of portfolio companies to withdraw their deposits at the same time is almost certainly not the right thing to do. And it is, of course, silly to take credit for a bailout that was certain to happen anyways. But as we will see, the mistake of the FDIC was not in bailing out SVB, but in extending unlimited insurance to all depositors everywhere.

Deposit Insurance as Financial Self-Harm

Our banking crisis is self-inflicted in long-running, structural ways. Deposit insurance, or liability insurance, has been blamed for an increase in bank failures. George Selgin has written about how prior to the Bank of Canada’s offering of deposit insurance in 1967, Canada had not suffered a bank failure since 1923.6 Failures since have been attributed to insurance.7 In the US, “empirical evidence – both historical and contemporary – supports the private-interest approach as liability insurance generally has been associated with increases, rather than decreases, in systemic risk.”8

This has been a consensus position in the economics literature for decades. Here is Paul Krugman writing in 1998 on the Savings and Loans crisis that claimed over 1,000 banks and thrifts in the 1980s. “It has long been known that financial intermediaries whose liabilities are guaranteed by the government pose a serious problem of moral hazard… depositors had no incentive to police the lending of the institutions in which they placed their money; since the owners of thrifts did not need to put much of their own money at risk, they had every incentive to play a game of heads I win, tails the taxpayer loses.”9

Some have objected to the idea that unlimited deposit insurance creates moral hazard. For example, Matt Levine argues in a recent column that the SVB bailout does not create moral hazard “for shareholders and executives and bondholders” who now “should be more concerned about risk-taking by your bank."10 Others, like Mosaic Ventures partner Benedict Evans instead claim that “parking your funds in a zero-interest [insured] deposit account does not have moral hazard” for depositors.11

For one thing, that shareholders were wiped out in the SVB bailout has no bearing on the question of moral hazard. Rather, as Scott Sumner eloquently summarizes the issue, moral hazard is about risk taking and decision-making. “Deposit insurance gives bank executive[s] an incentive to take socially excessive risks. In some cases the risks won’t pay off. But that doesn’t mean executives don’t have an incentive to take excessive risks.”12

Executives take excessive risks because the funds they get to invest are, if insured, risk-insensitive dollars from the Fed. They compete for this risk-insensitive leverage not by being better risk managers, but by luring depositors with advertisements, nicer offices, gifts, cheap mortgages, bad KYC, and fancy websites. Taxpayers should want bankers to be good risk-managers if we are giving them risk-insensitive dollars. Yet since they do not compete on risk-management we can hardly expect them to excel at it, and instead must try to force it through regulations and stress tests on which bankers have every incentive to cheat.

What about depositors, is it true there is no moral hazard because banks pay little interest on most deposits? For a supposed Silicon Valley expert, Evans seems to have never heard of Richard Serra’s insight that “if something is free, you’re the product.” Cash is not a zero carrying-cost asset. It costs money to custody assets on behalf of someone else. Those familiar with traditional or digital finance know that they must pay custody fees. How does Evans think that banks pay for running their business? It costs money to run a bank–we can pay fees, or we can pay by allowing bank executives to take risks with our money. There is no free lunch.

Evans and Levine also argue depositors do not suffer moral hazard because they cannot assess bank risks. In fact one might say, SVB depositors–including the top 10 accounts holding $13 billion–were totally clueless about the health of the bank. Sumner again has the perfect retort, “Clueless depositors are not evidence of a lack of moral hazard; they are evidence that moral hazard exists.” In fact, consumers assess quality all the time in nebulous markets. They never attend lectures at multiple universities but “know that Harvard and Stanford are better than South Dakota State and Western Michigan University.” In fact, consumers consistently outperform financial experts and central bankers at predicting inflation.

The worst part is that the moral hazard between depositors and bank executives is self-reinforcing. The economists at, of all places, the FDIC, have concluded that moral hazard is so strong that depositors will even increase insured (but not uninsured) deposits into failing banks! Moving the deposit insurance limit upwards only augments moral hazard. “While large, uninsured deposits provide depositor discipline through outflows, if banks can easily attract new insured deposits then there is little practical depositor discipline. Our results suggest that inflows into insured deposits are an important mechanism that weakens depositor discipline exerted by uninsured depositors.” Removing limits on deposit insurance, as we have just done, guarantees that there is no discipline left in the banking system at all.13

Payments, Not Deposit Insurance

You might now be convinced our banking system is bursting with moral hazard for both bankers and depositors. But you might object to putting depositors at risk. That argument might say that it is better to live in a world in which depositors never have to look at the quality of their bank.

First, that would be a normative claim about what banking regulation should do. Banking regulation as currently conceived is aimed at preventing financial contagion. It was not put in place to make life more convenient for depositors, whatever parallels Evans or Levine might want to draw between deposit and food safety.

Second, ensuring safe and sound payments for the average citizen has nothing to do with backstopping risk-taking by bankers. We simply have to separate payments and credit. In fact, Alipay already began doing something of the sort. Alipay does not pay interest to users that hold a balance, rather, it lets them invest in fixed-duration bundles of mortgages for 90 or 180 days. If even that is too risky, the American unbundling of payments and credit could require that each service be provided by separate institutions.

In short, because of moral hazard, unlimited deposit insurance is among the most expensive ways imaginable for providing simple payment services. Can we do better?

It seems unlikely within our current banking system. Economists have found that deposit insurance in many countries “has been installed as a pass-through subsidy targeted to particular classes of bank borrowers.”14 I have nothing against venture capital, and in fact have raised from VCs before. Still, the unlimited insurance granted to SVB depositors is an unearned subsidy at taxpayer expense, and sets a bad precedent. Expanding it to all banks only makes this worse. And yet it seems like the only logical conclusion after 70 years of cycling between ever larger government guarantees and ever larger bank failures.

The other alternative is the Financial Times’ Martin Sandbu argument that “any case for guaranteeing all deposits is a case for government provision of deposits.”15 In other words, if the federal government is going to be our indirect counterparty, we might as well bank at the Fed and cut out the commercial bank middlemen. But of course, it is far from certain that a state-owned bank would have been any good at servicing moonshot startups in the first place.

Regulatory Capture and Unintended Consequences

But the regulatory morass goes beyond the moral hazard of deposit insurance. Most regulation itself is so deeply informed by incumbent interests that the foundation of the entire regulatory structure is suspect. During the Ayr Bank Crisis of 1772, which threatened the Scottish and British financial system, Adam Smith wrote to Parliament “the commerce and industry of the country… cannot be altogether so secure, when they are thus, as it were, suspended upon the Daedalian wings of paper money, as when they travel about upon the solid ground of gold and silver.” He suggested three key regulatory safeguards–a prohibition on small-denomination bank notes, a cap on interest rates, and a prohibition on contingent liabilities. An unsuspecting reader would be forgiven for not knowing that these three regulations had already been in effect since 1765, and were the result of intense lobbying by the largest bankers of the day, many of them Smith’s lifelong friends. These regulations did nothing to make Scottish banking safer, but they did create a moat against smaller competitors.16

An old one-pound note issued by the Ayr Bank, also known as Douglas, Heron, and Co.

The Dodd-Frank Act, passed after the 2008 Great Financial Crisis, follows the same pattern. Rather than breaking up “too-big-to-fail” banks into smaller entities, the bill focused on managing the assets which banks hold on their balance sheets. As might be anticipated, this has made the banking system less robust. Tyler Goodspeed and Michael Faulkender have shown how the Dodd-Frank stress test regime might have individually made banks safer, but by making their balance sheets look similar made all banks vulnerable to systemic crises and regulatory errors.17

Central Banking is No Cure

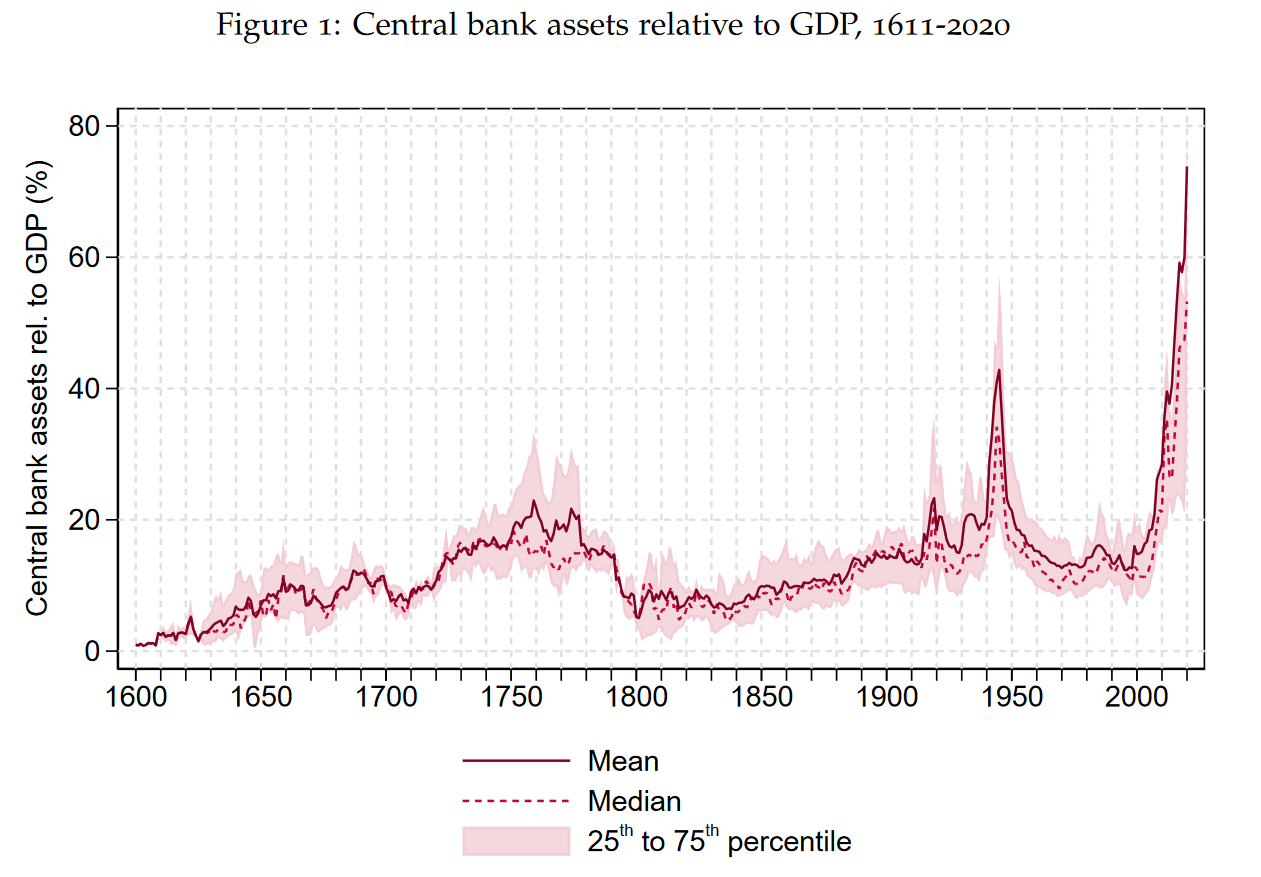

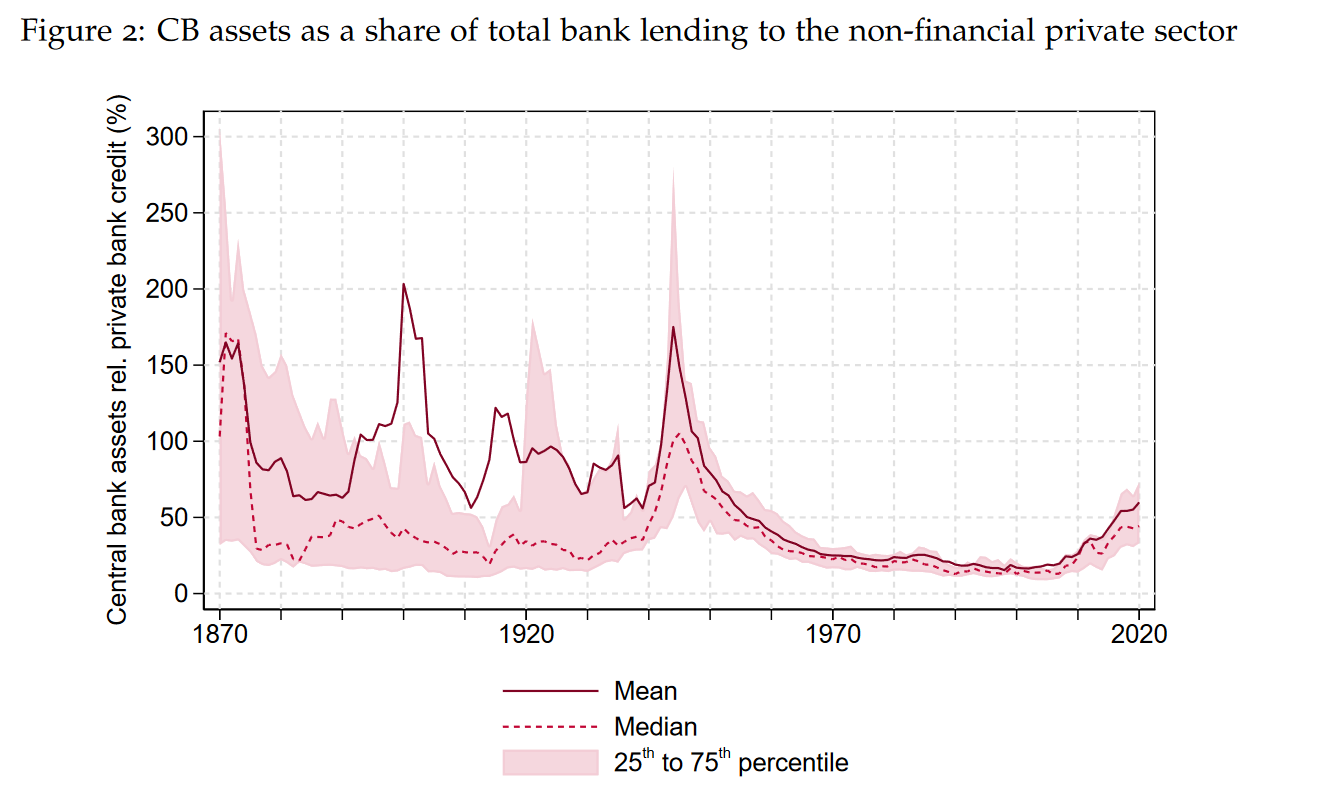

Even worse, while central bank liquidity might ameliorate a crisis, it increases the frequency and intensity of future crises. Niall Ferguson, Martin Kornejew, Paul Schmelzing, Moritz Schularick published a Hoover Institution working paper showing that over the very, very long run from 1587 to 2020, “liquidity support during financial crises has indeed tended to stabilize the economy successfully.”18 However, “the provision of central bank liquidity to financial markets raises the probability of future boom-bust episodes, pointing to potential moral hazard effects of central bank intervention.” Central bank balance sheets have ballooned relative to GDP (see above). Of course, central bank assets as a share of bank lending has shrunk because, given public support, total bank lending has grown even faster (see below).

Even setting interest rates, the “classical” tool of central bankers, is fraught with risk. Maximilian Grimm, Òscar Jordà, Moritz Schularick, and Alan M. Taylor published an NBER paper last month showing why, over the last 150 years, “when interest rates remain below the natural rate for an extended period of time, there is a build up in asset prices and in credit growth, both of which have been shown to be associated with greater financial fragility.” Specifically, “when stance is 1 percentage point (pp) lower on average in a 5-year window, then the probability of a financial crisis in the next 5 to 7 years increases by 5.5 pps, and by 15.5 pps in the following 7 to 9 years ahead.”19

Conclusion

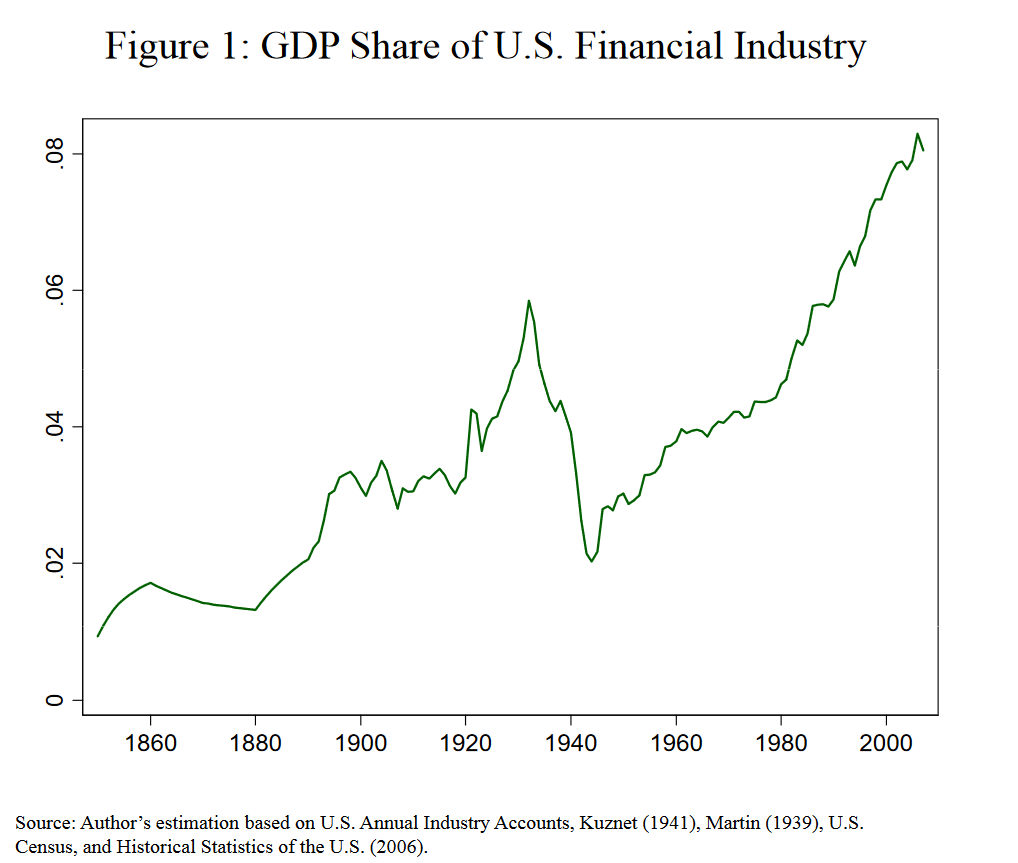

The inescapable consequences of banking might be more tolerable if we were not so intent on committing so many regulatory sins. Banking grows ever larger, propped up by public guarantees. Yet this only creates the structural conditions for larger crises. Over 130 years, finance’s share of GDP has increased eight-fold from 1% to over 8%, yet “the US financial system has become less efficient over time: the unit cost of intermediation is higher today than it was a century ago,” any gains in efficiency from information technology cancelled out by activities “whose social value is difficult to measure."20 Our banking system is much like California’s forests.21 By putting out all small fires for over a century, the US Forest Service allows fuel to build up for ever larger fires, to the point where the agency spends over half of its budget on fire suppression.22

Is there a way out?

Perhaps. Given the explosion in the size of the financial sector relative to the real economy, it is unrealistic that regulators will tolerate financial fires of any size. Reducing our exposure to banking crises would require financial regulators to carry out a politically fraught mission to reimpose capital controls and cut down the size of the financial sector.

But there might be another way. In the next two parts of this trilogy, I argue that the history of banking offers a clue to how to build the future of finance. Nature constantly attempts to evolve bank-like financial institutions, as financial intermediaries mix and match different financial services. Today, the rise of crypto and decentralized finance will unbundle the financial functions traditionally bundled together by today’s banks–payments and credit. More importantly, the disintermediated nature of DeFi frees us from having to bundle on the same balance sheet the unstable combination of payments and credit, of riskless liabilities and risky assets.

The Venerated Documents 尚書 is one of the Five Classics comprising the foundation of Chinese political thought, written during the Zhou dynasty (1046 BC – 256 BC) ↩︎

See, “Former FDIC chair: SVB ‘bailout’ was an ‘overreaction’” The Hill, March 21, 2023; Larry Summers on the SVB bailout. ↩︎

“Banks Lose Billions in Value After Tech Lender SVB Stumbles,” WSJ, March 9, 2023. Link↩︎

“Silicon Valley investors and founders express shock over SVB’s collapse, describe struggles to get money out,” CNBC, March 10, 2023. Link↩︎

“SVB run exposes rifts in chummy venture capital world,” Seattle Times. Link↩︎

Jack Carr, Frank Mathewson and Neil Quigley. “Stability in the Absence of Deposit Insurance: The Canadian Banking System, 1890-1966,” Journal of Money, Credit and Banking, Vol. 27, No. 4, Part 1 (Nov., 1995), pp. 1137-1158 ↩︎

Jack Carr, Frank Mathewson, and Neil Quigly. “The Economics of Canadian Deposit Insurance,” Department of Economics Research Reports, 9502. London, ON: Department of Economics, University of Western Ontario (1995) ↩︎

Charles W. Calomiris, Matthew Jaremski, “Deposit Insurance: Theories and Fact.” Working Paper 22223, May 2016 ↩︎

Paul Krugman. “What Happened to Asia?” January 1998. Link↩︎

Tyler Goodspeed. Legislating Instability: Adam Smith, Free Banking, and the Financial Crisis of 1772. Cambridge: Harvard University Press, 2016. ↩︎

Michael Faulkender and Tyler Goodspeed. “Want to Prevent SVB-Style Collapses? Scrap Dodd-Frank,” WSJ, March 20, 2023. Link↩︎

Niall Ferguson, Martin Kornejew, Paul Schmelzing, Moritz Schularick. “The Safety Net: Central Bank Balance Sheets and Financial Crises, 1587-2020,” Hoover Economics Working Paper 23102, February 3, 2023. ↩︎

Maximilian Grimm, Òscar Jordà, Moritz Schularick & Alan M. Taylor. " Loose Monetary Policy and Financial Instability,” NBER, Working Paper 30958. February 2023. Link↩︎

Thomas Philippon. “The Size of the U.S. Finance Industry: A Puzzle?” New York Federal Reserve, November 2011. Link↩︎

“Suppressing all fires has made the problem worse because now the forests and brush lands are unnaturally — and dangerously — overgrown.” See Kirk Siegler. “West Coast Fires: Climate, Forest Management, Lax Rules, Plenty Of Blame To Go Around,” NPR, September 15, 2020. Link↩︎

The USFS budget for 2018 was $4.73 B, while it spent $2.6 B on fire suppression. That year led to increases in the USFS budget, reaching $7.4 B in 2021, but the service still spent $3.7 B on fires that year. “Suppression Costs,” NIC. Link; “Budget and Performance,” Forest Service, USDA. Link↩︎