TL;DR: Great power financial sanctions, including currency reserve sequestration, have a long history. Financial authorities have a historically-tested playbook in response:

rebuilding financial reserves

ensuring domestic financial solvency

Both goals can be achieved by running an account surplus and imposing capital controls. In this light, worries that crypto could undermine financial sanctions against Russia are unfounded.

Crypto-for-oil is just commodity barter–it doesn’t move currency in and out of Russia. To undermine sanctions Russia would need to to 1) Bitcoinize/tokenize its domestic economy and financial sector or 2) acquire crypto for the CBR as a type of “digital gold”. Both these options are far too radical to be palatable to the Putin regime.

Introduction

Since the War on Terror, financial sanctions have become an American foreign policy superpower.1 Yet sanctions (or fear of sanctions) are not new. On April 10, 1940, the United States sanctioned Yugoslavia, an Axis ally. With Executive Order No. 8389, the US blocked access to $46.8 million in gold at the Federal Reserve Bank of New York and $13.6 million in private institutions.2

In the foothills of the first Cold War, the People’s Republic of China (PRC) sought to avoid the same fate. In 1950, just prior to the Korean War, the PRC moved its dollars out of New York and deposited $5 million with the Banque Commerciale pour l’Europe du Nord (BCEN), in the name of the Hungarian National Bank.3 Similarly, prior to the Soviet intervention in Hungary in 1956, “a Russian bureaucrat named Dregasovitch moved his country’s dollar balances to the Moscow Narodny Bank in London.” Reserves were also moved to the Narodny Bank in Paris, with technical assistance from Chase Bank.4

Staff of the Moscow Narodny Bank of London at their 20th anniversary dinner, 1939.

In response to Putin’s invasion of Ukraine, the US and its allies have again turned to financial sanctions, freezing Central Bank of Russia (CBR) reserves and cutting Russian banks from the SWIFT network. The irony is that despite Russian President Vladmir Putin’s assertion that he had made Russia “sanction-proof” by building up Russia’s reserves after 2014, he failed to grasp what lowly Dregasovitch understood so well—that it is not enough to “own” big foreign exchange reserves, it is just as important to make sure they are safe from confiscation.

As SWIFT sanctions begin to take effect, some commentators and regulators have begun to ask if crypto undermines financial sanctions against Russia. The answer is no. Using crypto tokens in international trade is the same as barter—exporters still need a way to convert a digital commodity into currency. They could sell tokens inside Russia, much as they could sell any other commodity. But this would not solve Russia’s country-level inability to move currency in and out of the country.

Bypassing sanctions requires a radical transformation. Russia would need to Bitcoinize or tokenize domestic economy and financial sector; that is, Russia would have to allow tokens as legal tender on par with the ruble.

History suggests this is incredibly unlikely. In fact, the CBR’s efforts are straight out of the history books—it is imposing capital controls and mandating exporters to turn over surplus dollars. That is because Russia’s financial problems are the classic problems of war finance—how to rebuild reserves and how to keep solvent domestic financial institutions. Monetizing crypto would undermine this playbook.

Nonetheless, Western regulators will continue raising a false alarm over crypto and sanctions as they seek to leverage the crisis to increase their domestic control over crypto exchanges and limit access to decentralized finance (DeFi). In the contest between great powers, crypto has no impact. But crypto adoption does hinder surveillance-happy regimes from crushing dissent and protest, as Canadian Prime Minister Justin Trudeau recently did by sanctioning individuals who had donated to the Ottowa trucker convoy. It is hard to ignore that crypto and sanctions are a distraction from the one thing the US and its Europeans allies can do to further hobble Russia’s financial system—stop buying cheap Russian gas and oil.

CBR sanctions

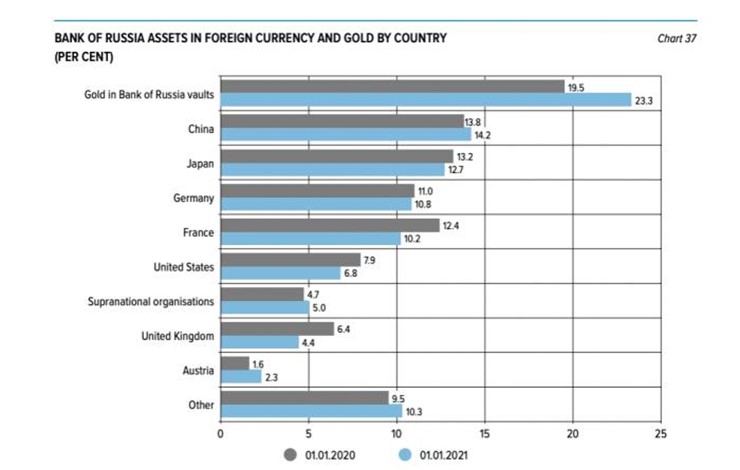

The CBR certainly tried to hedge its bets against sanctions by building up a massive amount of reserves, selling off dollars, and accumulating physical gold inside Russia. Nonetheless, it was still exposed to sanctions by US allies, as its own annual report made clear.

Russia’s central bank has likely lost access to a majority of its reserves. It still has control of its own gold, claims in supranational organizations (like the IMF), and its reserves in China. This leaves access to only 42.5% of its reserves.

Kicked out from SWIFT

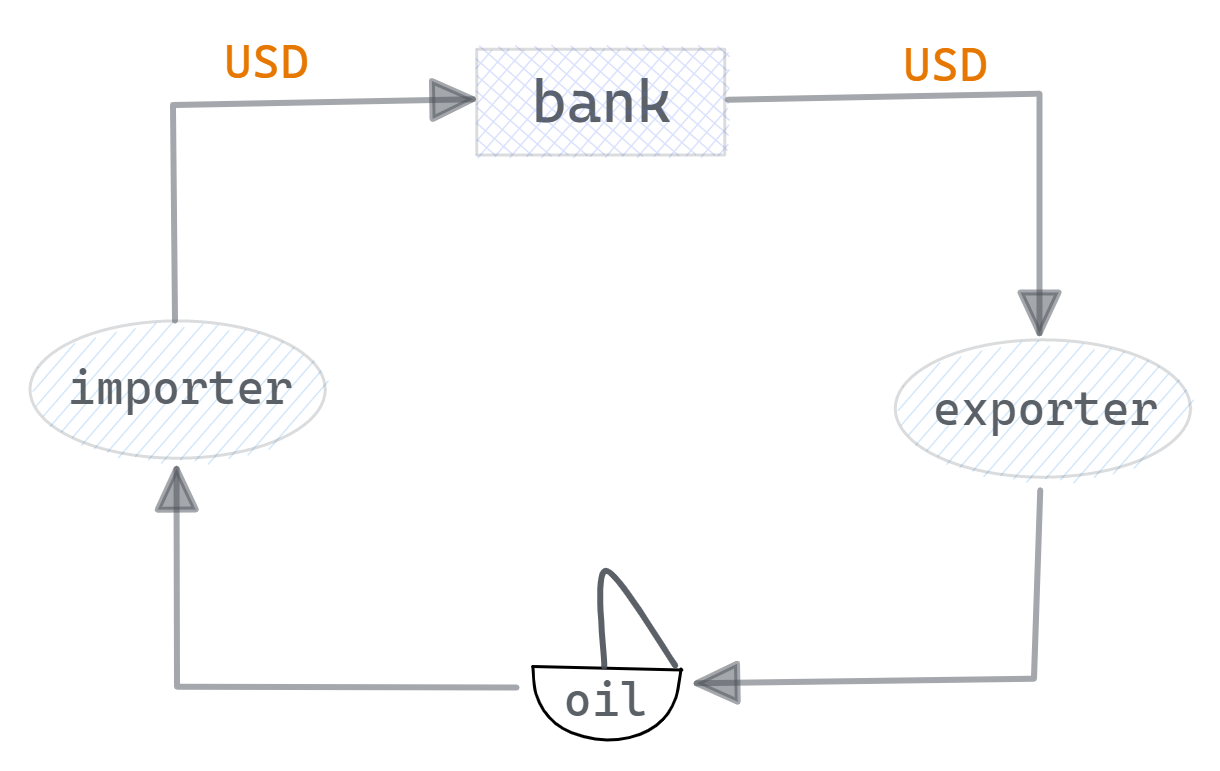

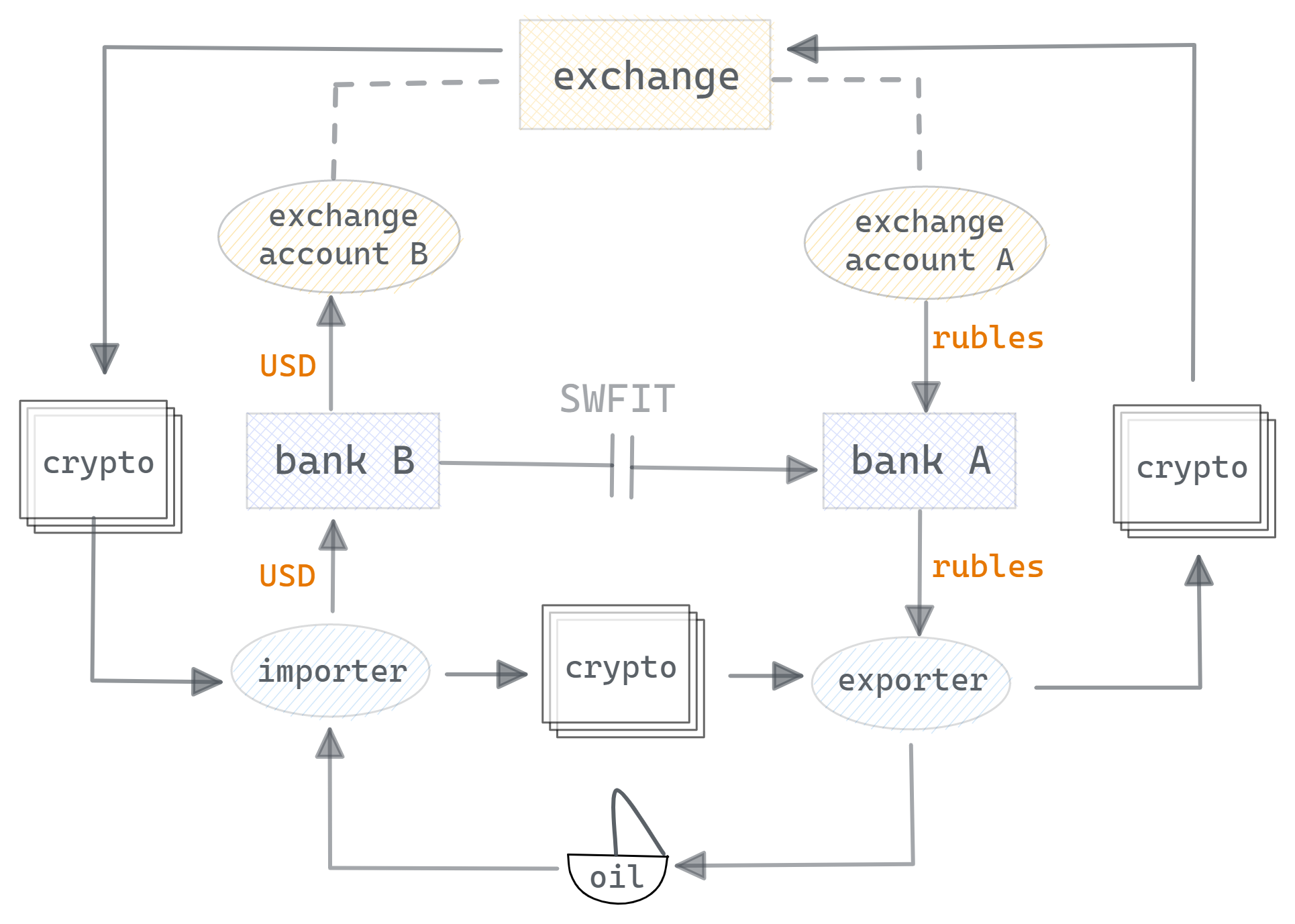

The second piece of the financial offensive against Russia is exclusion from SWIFT. SWIFT is a communications protocol between banks used to execute of international transfers. Here is how it works. In a domestic transaction, unless a trade is executed in cash, payment for goods and services involves crediting and debiting the bank accounts of sellers and buyers.

But what if the buyer and seller are in different countries? (Assume for simplicity that the exporter’s domestic bank only offers ruble accounts, and the importer’s bank only offers dollar accounts.) In these cases the importer asks their bank to route funds to the exporter’s bank. Excluding Russia from SWIFT makes this near impossible. However, one could say, the Russian oil exporter can still get paid if they have an account outside of Russia.

This is a temporary solution. The exporter will accumulate USD or EUR in their non-Russian bank account, but will be unable to service RUB obligations in Russia owed to workers and other providers.

As Credit Suisse analyst Zoltan Pozsar pointed out in his recent dispatch, “If you jam the flows by making banks unable to receive and send payments, you have a problem, much like when a tri-party clearing bank did not return cash to money funds for fear of ending up with an intraday exposure to Lehman.” Without extraordinary intervention from the CBR, SWIFT sanctions would lead to an accumulation of missed payments and potential insolvency.5

Scaremongering for clout

It is no surprise to find commentators raising alarm that Russia could use crypto to bypass sanctions. Consider former Facebook executive Alex Stamos’s sensationalist suggestion that NFTs can allow Russia to launder the money made from selling oil.6 Or the recent New York Times article, which gestured towards vague means of hiding blockchain transactions. The reporters did not describe these methods, as it was based solely on a third-hand reference to a still-unpublished report from 2018.7

Despite their origins in social media attention markets, could there be any truth to these allegations?

Crypto is useless against SWIFT sanctions

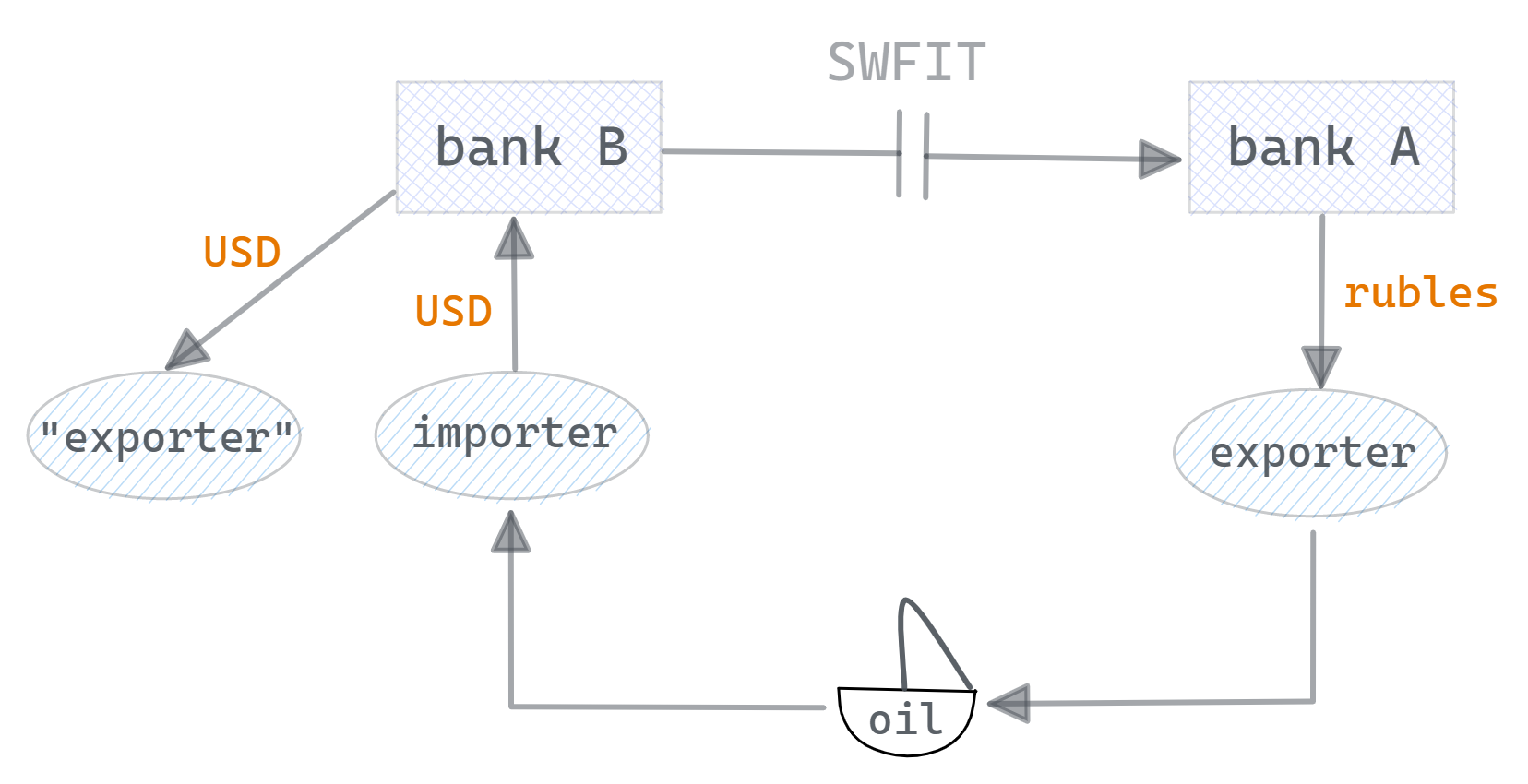

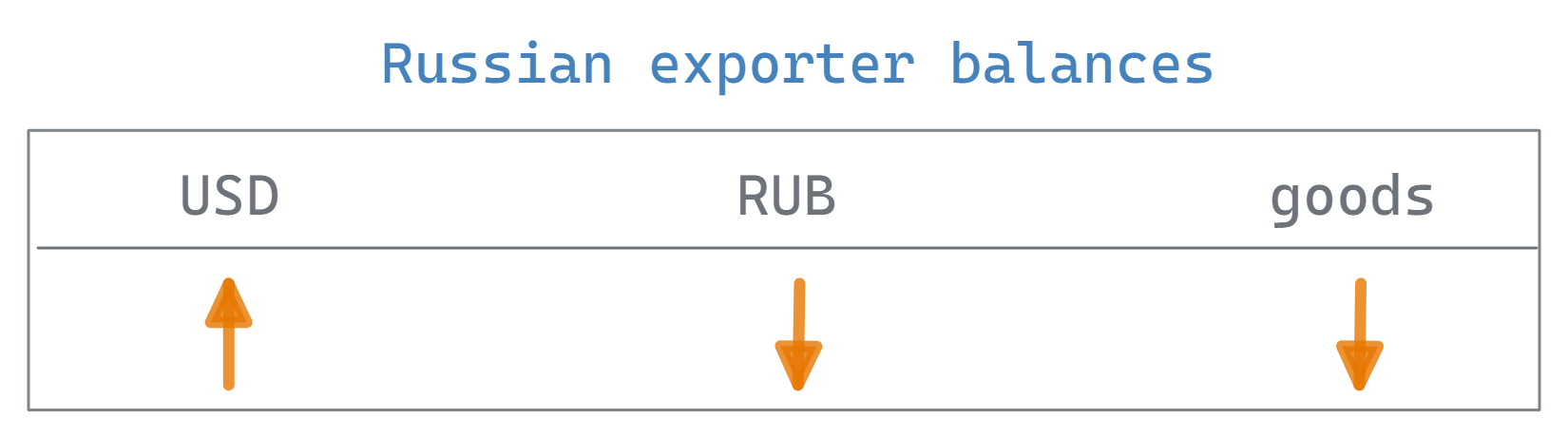

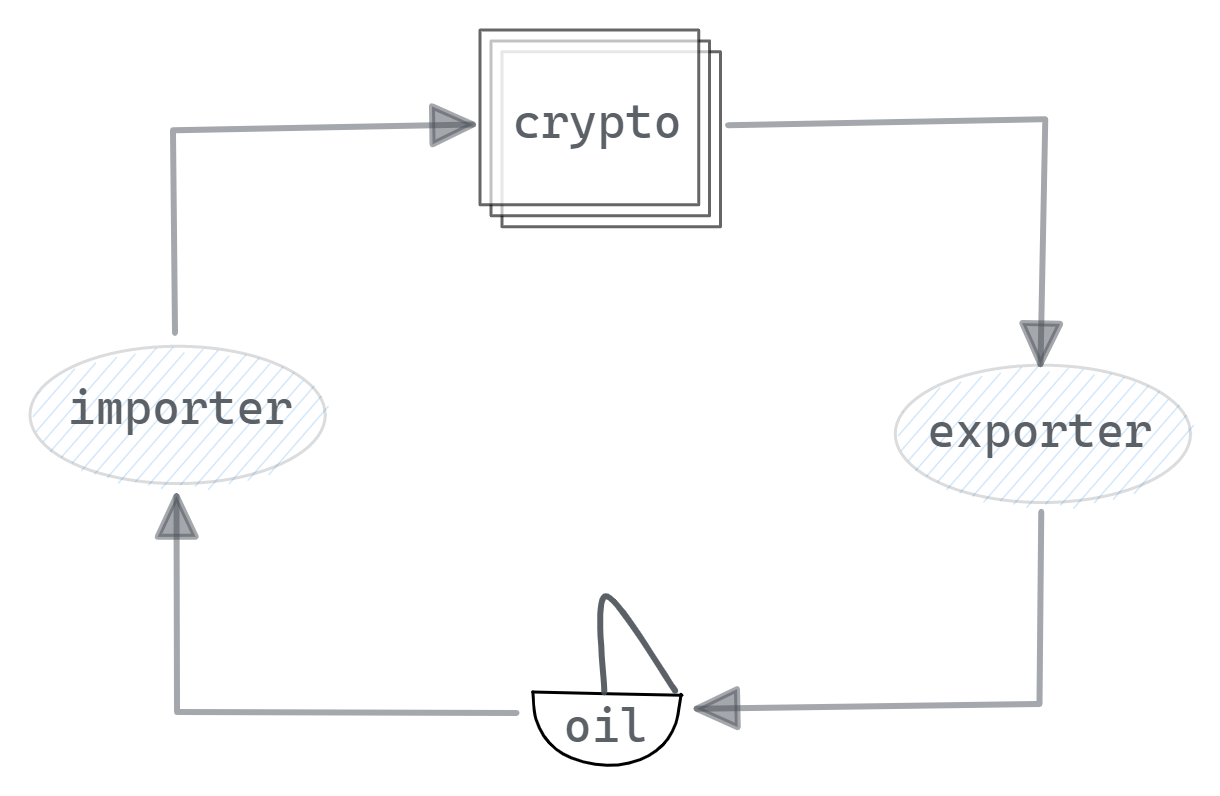

Crypto at first seems to provide a way to bypass SWIFT sanctions. An importer can “pay” Russian exporters or citizens directly. But this is dead wrong! Crypto tokens are not money, they are commodities. Paying with tokens is the same as paying in any other commodity like diamonds or corn—it is a form of barter.

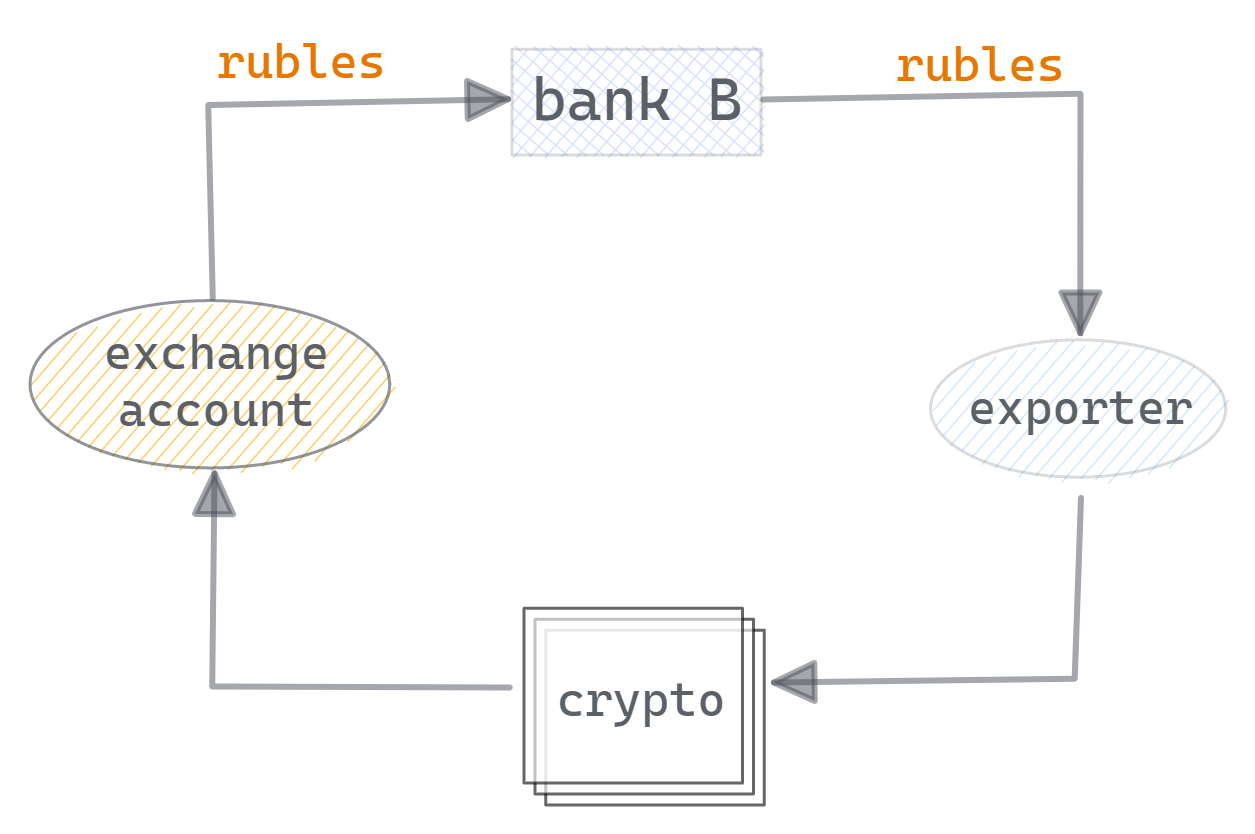

Russian entities still need sell these commodities for currency to service their obligations. Centralized exchanges are one such place to sell crypto. They have local bank accounts and can make transfers to users of the same nationality. It appears that a cross-border transfer has happened. The exchange would be selling crypto to a European importer and buying it back from a Russian exporter.

However, this is too good to be true. Exchanges are just other users of the banking system. Users don’t “withdraw” funds from exchanges directly. Rather, the exchange’s local bank transfers funds to the user’s bank account. But exchanges can only off-ramp a limited number of users before depleting the cash in their bank accounts. And a SWIFT exclusion prevents them from replenishing their Russian account with funds from their non-Russian banks. Thus, a “run on the ruble” through exchanges will cause exchanges to stop processing bank withdrawals. The balance sheet problem to the exchange, which accumulates currency in its non-Russian account as its Russian account is drained of currency.

Just as obviously, there is no way to meet Russian exchange needs by draining the meager currency in crypto exchange bank accounts. Russian exports are over half a trillion dollars every year, and Russia runs a trade surplus of around $100 billion. Russian reserves, at the beginning of the current war, were about $630 billion

The reality is that Russia cannot use crypto or DeFi to bypass sanctions. Exchanging tokens for oil is just commodity barter by another name, when what the CBR needs is currency reserves to ensure the stability the Russian financial system.

What is to be done?

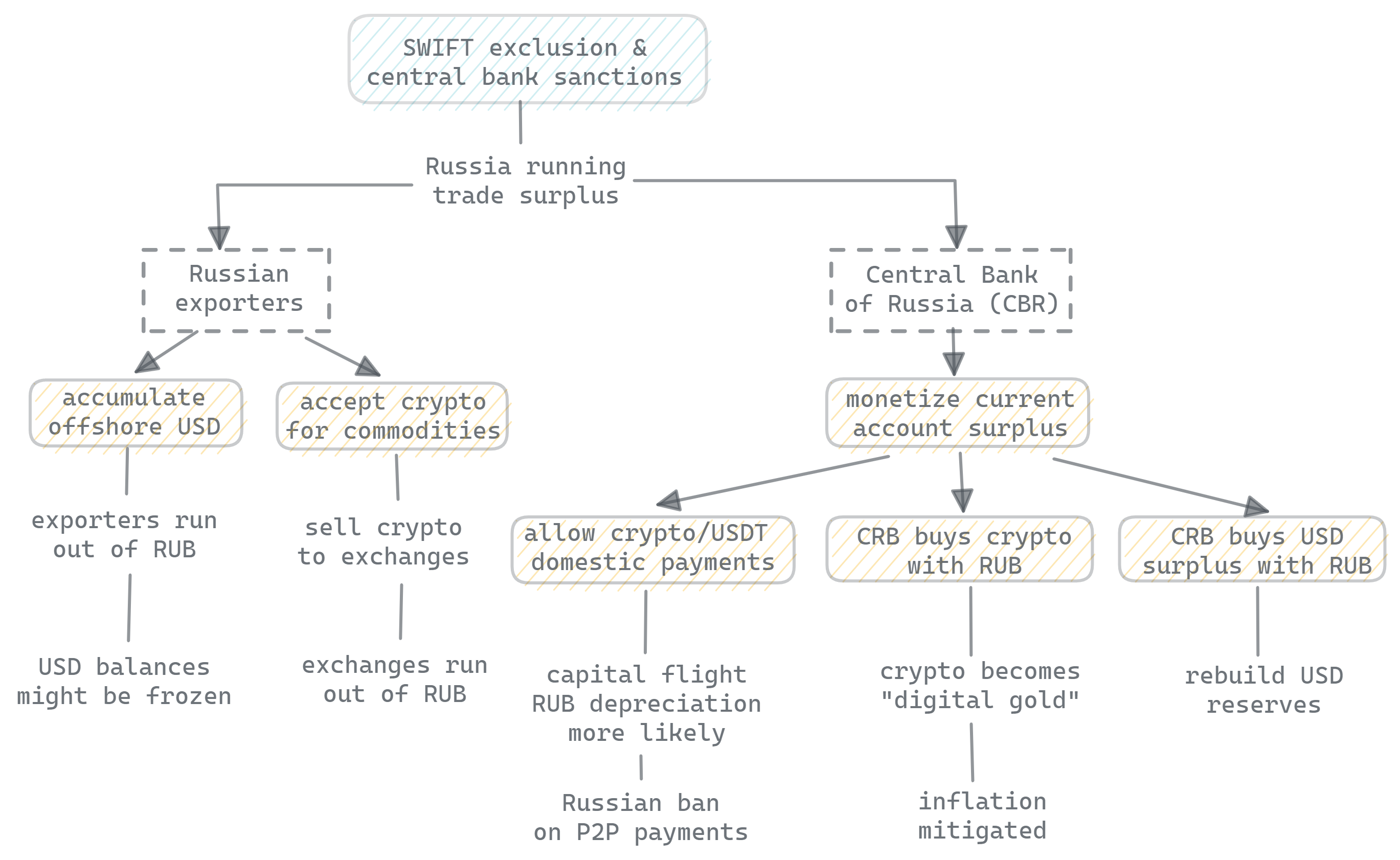

So what is the Central Bank of Russia to do? As long as Russian oil continues to flow on international markets, history suggests two options—imposing capital controls, or making crypto tokens legal tender.

Already the CBR is poised to force Russian importers to sell their FX earnings, helping it to rebuild its reserves. Following the Chinese example, the Russians can also try to “sterilize” these actions by issuing bonds domestically to soak up excess RUB, mitigate inflation, and soften the desire for capital flight.

This approach resembles some of the policies pursued after World War II. Britain attempted to protect its currency reserves by controlling the movement of capital out of the sterling area, starting with the Defense Regulation of 1939 and continuing with the 1947 Exchange Control Act. After 1944 the Bretton Woods system standardized thee measures, putting capital and exchange controls in place to prevent the excessive outflow of precious dollar, sterling, and gold reserves.

A second, much more radical approach would be to make crypto legal tender—that is, to Bitcoinize or tokenize the economy and financial system. Russians receiving Bitcoin or stablecoins like Tether’s USDT would then be receiving money, not a commodity.

However, such a transformation would be unprecedented, as it makes war finance harder, not easier. War time is just the time when governments use inconvertible fiat currency to finance themselves. Almost all governments abandoned gold convertibility during WWII. Republican China made paper money the sole legal tender in 1935.

More importantly, as the weaker party against the West, tokenization would make capital flight so easy as to be virtually impossible to stop. In other words, Bitcoinization and tokenization might very well be a boon for Russian citizens, but it would hamstring their governments efforts to financially mobilize for war. This isn’t lost on the Russian authorities, which are poised to peer-to-peer token payments in Russia.

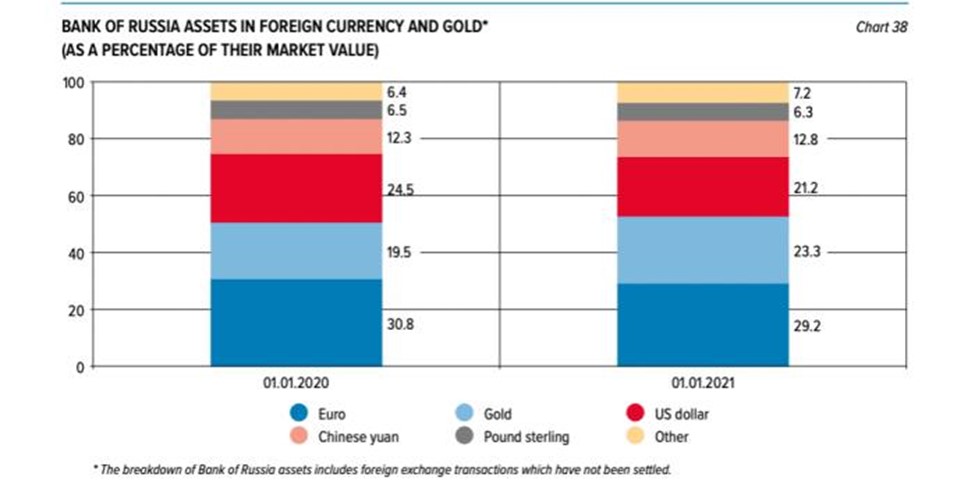

This leaves a third option. Rather than purchase its exporters’ dollars, Russia could opt to purchase their Bitcoin, thereby christening Bitcoin as “digital gold.” Russia holds more actual gold as a monetary reserve than it does of any other currency save the Euro. Its gold reserves have more than doubled since 2014, from about $50 billion to $132 billion. In comparison, the CBR holds $468 billion in foreign exchange, $24 billion in SDRs, and $5 billion at the IMF.8

There are some risks, of course. Any hint that Russia is accumulating Bitcoin or other tokens would lead to a speculative spike in price. Selling might be just as disruptive. But digital gold has one important advantage over regular gold—it is much harder to confiscate.

Conclusion

Restricting access to crypto and decentralized finance (DeFi) has little to do with great power conflicts and much to do with petty domestic tyrants. But this will not keep regulators, journalists, and police forces from capitalizing on the question of crypto and sanctions to increase their control and surveillance. Crypto-skeptics like Stamos thus, perhaps unwittingly, advance an agenda that would allow the financial sanctioning and de-platforming of domestic protesters and dissent. The freezing of financial accounts of Canadians that donated to the trucker convoy protesters is a vivid example of these dangers.

For Russia itself, capital and exchange controls will be the preferred tools for preserving financial stability. The only way to bypass SWIFT sanctions would be to allow Bitcoin or crypto tokens to serve as legal tender. Given that Russia just banned P2P crypto payments, this seems unlikely. More importantly, war is when governments rely the most on inconvertible fiat money to finance their armies and stem capital flight.

In a conflict between great powers, central banks are still crucial to preserving financial stability and funding the government during wartime. Giving up control of the domestic financial system is the last thing Russians are likely to do.

Putin was not as clever as Dregasovitch in preserving Russia’s currency reserves. But unlike the Yugoslavs in 1940, he was at least clever enough to keep Russian gold in Russia. So it is not inconceivable that in a future conflict we might discover that central banks have been holding a little bit of “digital gold” too.

Sahil Mahtani. “Carrie Lam’s Problem—and Ours: China’s State-Backed Digital Currency.” American Affairs Journal. URL↩︎

Memorandum by the Chief of the Division of Southern European Affairs (Barbour) to the Under Secretary of State (Lovett), [Washington,] January 7, 1948. Foreign Relations of the United States, 1948, Eastern Europe; The Soviet Union, Volume IV. URL↩︎

H. M. Wachtel. The Money Mandarins. London: Pluto Press, 1990. ↩︎

Gary Burn. “The State, the City, and the Euromarkets,” Revie of International Political Economy, Summer 1999. 254; M. Mayer. The Bankers, London: W. H. Allen, 1976. ↩︎